It's happened to all of us.

The neighbour's dog barking in the distance wakes you up. Come on, it's 2 a.m., and you need to get up early. It takes a moment to place it because you're groggy and disoriented. It's the neighbour's dog, right?

It isn't. He's yours, and he's been out in the dark for hours.

The feeling that follows isn't just about the dog. It's the compound weight of being completely certain about something that turned out to be entirely wrong: embarrassment, responsibility, and more than a little guilt. You had assumed someone else let him in. It seemed so logical at the time.

Assumptions can be dangerous, especially when animals are involved. But the assumptions that can really cost you aren't always the ones you make in the kennel. Sometimes they're the ones you make before you open the doors.

When I purchased my kennel, I made an assumption that took a while to find. When I found it, that same feeling hit. First embarrassment and then guilt. I should have known better.

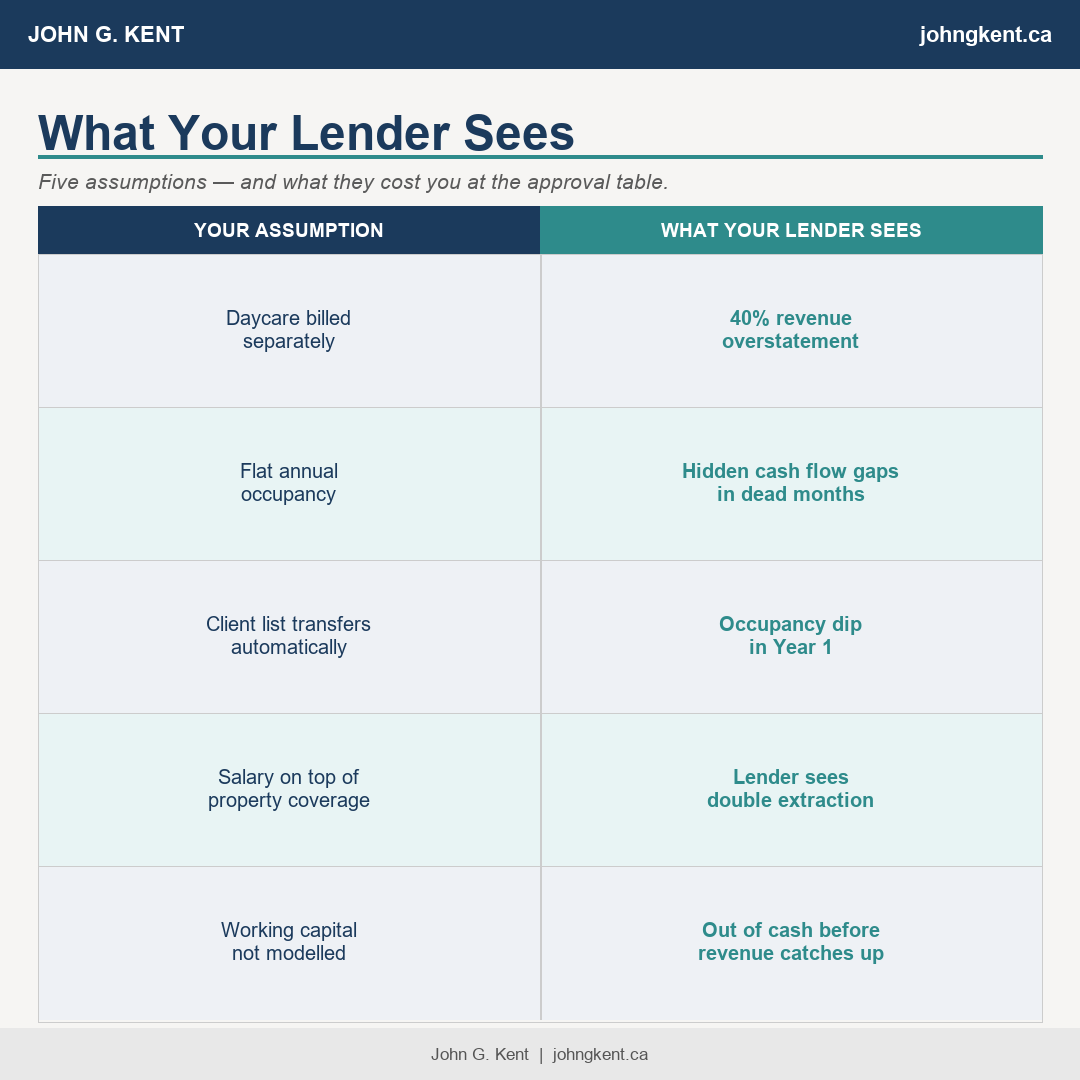

I assumed daycare was billed separately from the overnight rate. It seemed logical. A dog stays overnight and participates in daycare during the day — of course, that's two billable services. The rates today are $45 for overnight and $30 for daycare. The napkin model charges $75 per boarding dog. The honest model puts $45. That's a 40% overstatement on every single dog in the projection, and at the time, our numbers weren't far off. The rates have changed since we bought the kennel, but the math works the same way. I caught it before it cost me the purchase, but what I wasn't prepared for was the feeling that came with finding it. The same embarrassment from two in the morning. The same stomach drop when I realised and then asked myself, "What else did I wrongly assume?"

Finding it wasn't relief. It was heartburn. That immediate, stomach-churning moment of oh my god, what did I just do. Because it isn't just about the approval anymore, it's the questions that stem from the failure. Was the kennel viable? Should I even be approved? And once that door opens, you go down the rabbit hole — double, triple, quadruple checking every number on the page. Are these real? What other mistakes could I have made?

Can we actually afford this? Because this isn't a business plan anymore. This is the rest of our lives.

There are many assumptions people make when they're looking to purchase a kennel. Here are some of the most expensive ones you should steer clear of.