Business

What A Professional Lender Is Actually Measuring: A Kennel Buyer’s Guide to the 6 C’s of Credit

Sitting across from a professional lender feels like an interrogation. Here’s what they’re actually measuring — and how to walk in speaking their language.

By John Kent · June 7, 2026 · 13 min read

TL;DR

- When a lender asks those hard questions, they’re running six lenses called the 6 C’s of Credit. Every kennel buyer faces them whether they know it or not.

- Your projections aren’t just numbers — they’re a personality test. Stress-tested forecasts tell the lender who you are before you say a word.

- Kennel applications often get treated like farm applications. Understanding why is the first step toward having an intelligent conversation about where that framework doesn’t fit.

- Appraised value and forced-sale value are two different numbers. Most kennel buyers don’t understand the gap until they’re in it.

You’ve done the research. You know the industry is growing. You know Canadians love their dogs. You’ve walked through kennels, run the numbers, and maybe even found the property. You’re ready.

Then you sit across from a professional lender.

The questions start coming, and something shifts. They’re not asking about your passion for dogs. They’re not impressed by the market statistics you printed out. They’re asking about things that feel sideways to the conversation you came to have. Debt service ratios. Declared income. Forced sale value. Personal guarantees.

You walked in prepared. You felt like any question thrown your way was only going to be a softball. The questions didn’t feel like softballs. They felt like arrows aimed at tearing your sails apart.

You leave the meeting feeling like they weren’t listening. Like they didn’t understand what you’re trying to build. Like they aren’t your friend, but your enemy.

Here’s what I want to tell you, from someone who has sat on both sides of that desk.

They were listening to every word. They just weren’t hearing what you were saying. They were hearing something else entirely.

With this translation guide, you’ll walk into any banking conversation speaking the lender’s language. And that changes everything.

Who’s Talking to You

My name is John Kent. My background in finance dates back many decades, to when I earned my Bachelor of Commerce from the University of Toronto. From there, I moved into banking as a business advisor at Scotiabank, where I sat across from small business owners exactly like you, evaluating applications, asking the questions that felt like arrows. After the bank, I managed parts at a New Holland dealership, where agricultural financing was a daily conversation.

Then I became the kennel buyer.

In 2016, Veronica and I purchased the Oasis Pet Hotel in Bath, Ontario, and renamed it The Loyalist Barkway. We paid $285,000 for a neglected property that appraised at $493,000 within ten months. As of May 2022, that same property was valued at $1,197,000.

That value growth didn’t happen by accident. It happened because we made purposeful decisions about our investment. We worked where we could, invested in ways to increase income, and sought opportunities whenever possible.

When it came to the financing, my experience at the bank taught me how to speak like a lender. It showed me what a lender is measuring when they ask those hard questions. In retrospect, it also taught me which tools most Canadian kennel buyers are unaware of.

What follows is what I have put together after reading the same requests over and over on social media. It’s what I wish every kennel buyer could learn before walking into their first bank meeting.

The Framework Nobody Shows You

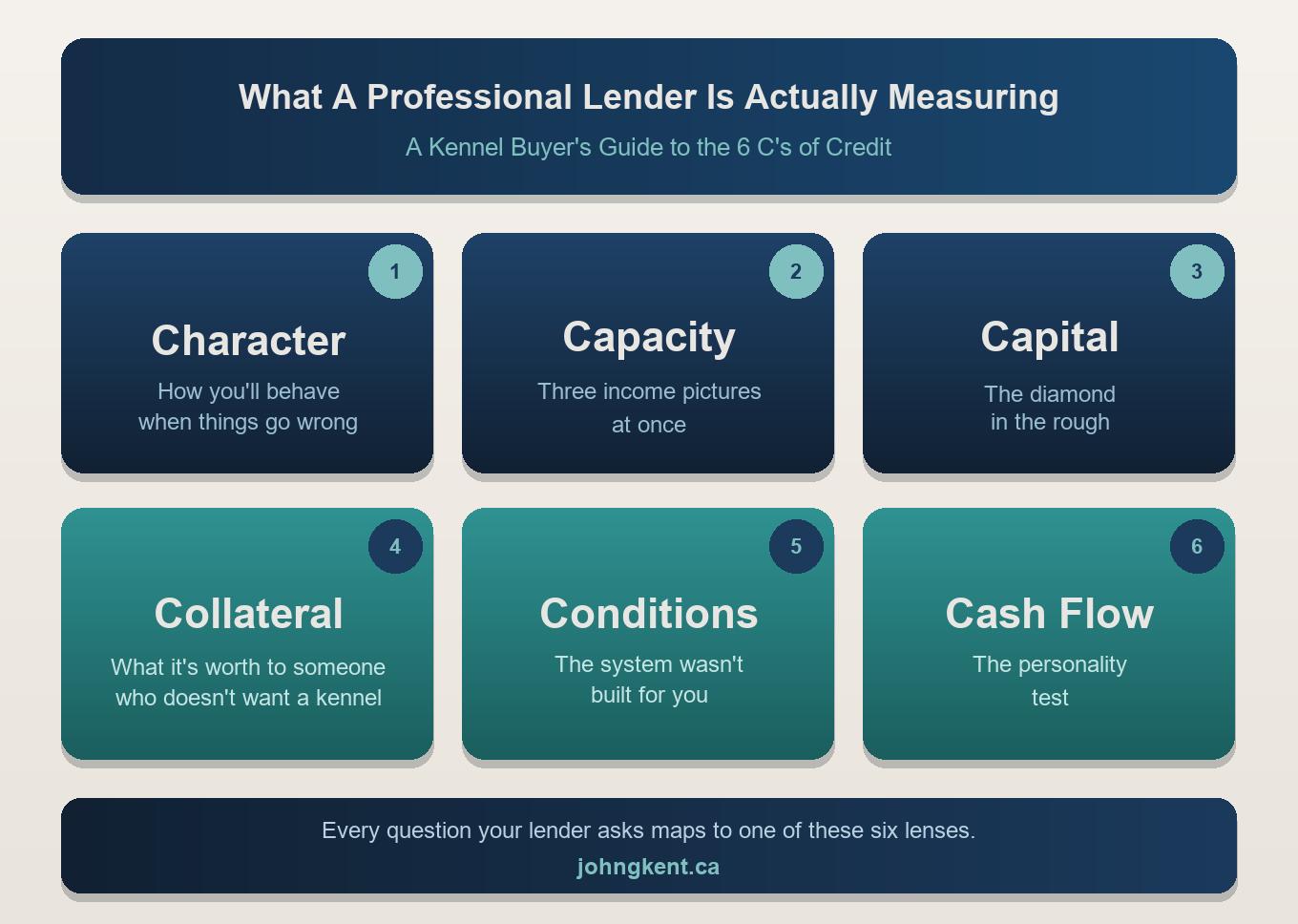

When a lender evaluates your application, they aren’t working from a gut feeling. They’re working from a framework with six specific lenses that assess every deal that crosses their desk.

They’re called the 6 C’s of credit: Character, Capacity, Capital, Collateral, Conditions, and Cash Flow.

You won’t find them on an application form, and nobody is handing out free checklists. But they’re present in every question the lender asks and in every document they request.

Here’s what most guides won’t tell you. There is a hidden meaning to each element. And in a kennel acquisition, each one carries complications that most lenders are wary of because most buyers never anticipate them.

This is what they’re actually measuring.

Six lenses. Every question your lender asks maps to one of them.

Character: How You’ll Behave When Things Go Wrong

Character is the C that feels the most personal, and it is, but not in the way most people think.

When a lender assesses your Character, they aren’t asking whether you’re a good person. They’re asking a harder question about how you’re going to behave when things go wrong, because things always go wrong at some point. Not always dramatically, but a slow season, an unexpected repair, a staff problem, or a health issue will test every operator eventually. Lenders have seen enough deals to know that the difference between a borrower who works through difficulty and one who walks away often has nothing to do with the size of the problem and everything to do with the person sitting across the desk.

Character shows up in your credit history, but it also shows up in how you present yourself, how prepared you are, how honest you are about your own weaknesses, and perhaps most revealingly, in how you build your financial projections.

An optimist builds to the upside and hopes for the best, while a pessimist plays it safe. Still, a prepared operator tests both ends of the scale, presents a stress-tested framework, and shows the lender they’ve already had the hard conversation with themselves before walking into the room.

Our article on Budget Assumptions walks through the whole framework so you can build projections that actually show the lender who you are.

Capacity: Three Income Pictures at Once

Capacity boils down to one very important prospect. Can you pay this back?

For a personal loan or a car payment, that’s a relatively straightforward calculation. Still, for a kennel acquisition, you’re asking the lender to evaluate the existing business income, your envisioned capacity from the changes you plan to make, and your household income from outside the business, then make sense of how all three interact.

Each element adds its own complexity, not to mention the complexity created by interactions among the three. Together, however, they create a financial portrait that’s more complex than most buyers anticipate.

Capital: The Diamond in the Rough

Most buyers think about capital as fixed numbers. How much money do I have? How much money does the lender require? And does it add up to a successful purchase? While those are important, there are hidden elements to explore. What can you see that other buyers can’t? Because in a kennel acquisition, capital isn’t always obvious.

The Oasis Pet Hotel was tired when Veronica and I made our initial offer. We identified opportunities to improve and, within ten months of doing the work ourselves, the property appraised at $493,000 against a purchase price of $285,000. As of May 2022, it was valued at $1,197,000. That gap between what a neglected property is worth today and what a motivated operator can build it into is where capital gets created.

Collateral: What It’s Worth to Someone Who Doesn’t Want a Kennel

Collateral is the C where kennel buyers most consistently overestimate their position. When your property is appraised, the value reflects what a motivated buyer would pay under normal market conditions. The lender is simultaneously running a quieter calculation of what this asset is worth in a distressed scenario for whoever they can find quickly. In a kennel, those two numbers can be very far apart.

The more kennel-specific your build-out, the narrower the pool of buyers who would want it as-is. My neighbour’s property was listed for sale by the lender as of this writing. That outcome is never the plan, but it happens. Understanding what drives the gap between appraised value and forced-sale value is one of the most important things a kennel buyer can learn before building, renovating, or refinancing.

Conditions: The System Wasn’t Built for You

Of all the C’s, Conditions is the one that operates most invisibly, because it describes the external environment your application lands in rather than anything you’ve done or can control. It covers the economic climate, the industry outlook, and the regulatory framework that surrounds your specific type of business.

For kennel operators in Canada, Conditions carries a complication that most buyers never see coming.

A boarding kennel that includes a residence on rural acreage, which describes the majority of licensed kennels in Ontario, given the provincial licensing requirements, looks a great deal like a farm on paper. The same structure, the same asset profile, the same inseparability of the personal and the professional that makes farming what it is. Canadian lenders, including some of the major chartered banks, have historically treated kennel applications like farm applications for exactly this reason. This means your income may be evaluated against assumptions built for a business whose revenue depends on the weather, commodity prices, and biological cycles rather than the relationship-driven, year-round demand model that actually describes what you’re running.

This isn’t arbitrary. It’s the closest framework the system has for a business where the commercial operation and the family home are one asset, one debt, and one family’s livelihood. Understanding why the lender reaches for that framework is the first step toward having an intelligent conversation about where it applies to your situation and where it doesn’t.

The landscape is shifting. Whether that shift is happening at the policy level or the relationship manager level is a question worth asking your lender directly, because the answer should change how you negotiate.

Cash Flow: The Personality Test

Your projections are the most honest thing you’ll put on that lender’s desk, whether you intend them to be or not.

Most applicants bring optimistic projections, not because they’re being dishonest, but because they develop a blind spot in their excitement to get on with the actual work. Lenders have reviewed enough projections to recognize the pattern immediately, and an optimistic projection from a first-time kennel buyer doesn’t signal confidence. It signals that the applicant hasn’t yet had the hard conversation with themselves.

While it’s nice for the lender to know how much your kennel could earn in a good year, they’d rather know how well you can service the debt in a difficult one. A projection that tests both assumptions tells a completely different story about the person who built it than a single optimistic column of numbers.

Our Budget Assumptions article dives deep into how to build projections that reflect the economic reality rather than hopes and dreams, including the framework I built for our own acquisition that stress-tested both ends of the scale and told the lender exactly the kind of operator they were dealing with. If you want to pressure-test your own numbers before that conversation, the Kennel Startup Budget Calculator walks you through the same framework interactively.

Use the interactive Kennel Startup Budget Calculator to pressure-test your projections before your lender meeting — the same framework John Kent used for the Barkway acquisition.

Try the Kennel Startup Budget CalculatorWhat This All Adds Up To

Six lenses. Six questions the lender is asking before, during, and after every conversation you have with them. And running beneath all six of them, a single question they never ask out loud but are always trying to answer.

Are you worth the risk?

Not your kennel. Not the property. Not the market. You.

Your Character predicts how you’ll behave when it gets hard. Your Capacity determines whether the numbers actually work. Your Capital reveals whether you can see opportunity where others see problems. Your Collateral tells them what they’re holding if things go sideways. Your Conditions describe the environment your business operates in and whether the system understands how to evaluate it. Your Cash Flow shows them who you are before you’ve said a single word about your dream.

Every question in this guide is ultimately a question about yourself. The good news is that creating a to-do list for finances is easy. The operator who works through that list before walking into the lender is fundamentally different from the one who walks in with passion alone.

More than half of Canadian households own at least one pet, according to the Canadian Animal Health Institute. The demand is real. The industry is growing. Lenders aren’t disputing any of that. They’re asking whether you, specifically, are the right person to build a business inside it.

Before you walk into that meeting, make sure you can answer yes.

The numbers you bring to that meeting matter as much as the answers you give. The Kennel Startup Budget Calculator builds the financial picture your lender needs to see, with a built-in stress test.

The numbers you bring to that meeting matter as much as the answers you give. Build the financial picture your lender needs to see — with a built-in stress test.

Build Your Numbers Before the Meeting

About the Author

John Kent

John Kent is a kennel operator, former Scotiabank business advisor, and co-owner of Loyalist Barkway in Bath, Ontario. He founded JGK Academy to share what he learned on both sides of the lender’s desk.

In This Article

- Who’s Talking to You

- The Framework

- Character

- Capacity

- Capital

- Collateral

- Conditions

- Cash Flow

- What This All Adds Up To

Finance Hub

- Hub What A Professional Lender Is Actually Measuring You are here

- Budget Assumptions

- Before You Borrow